Top 5 Updates from Gold Price FintechZoom

In this article, we delve into the most recent and significant changes in the gold market, all curated from FintechZoom. Whether you’re an investor, trader, or simply interested in precious metals, our comprehensive updates will provide you with valuable insights and trends. Join us as we explore the top 5 gold price movements and what they mean for the future of the market. Don’t miss out on these crucial updates from Gold Price FintechZoom!

Central bank Insights On Gold Price FintechZoom – March 2024

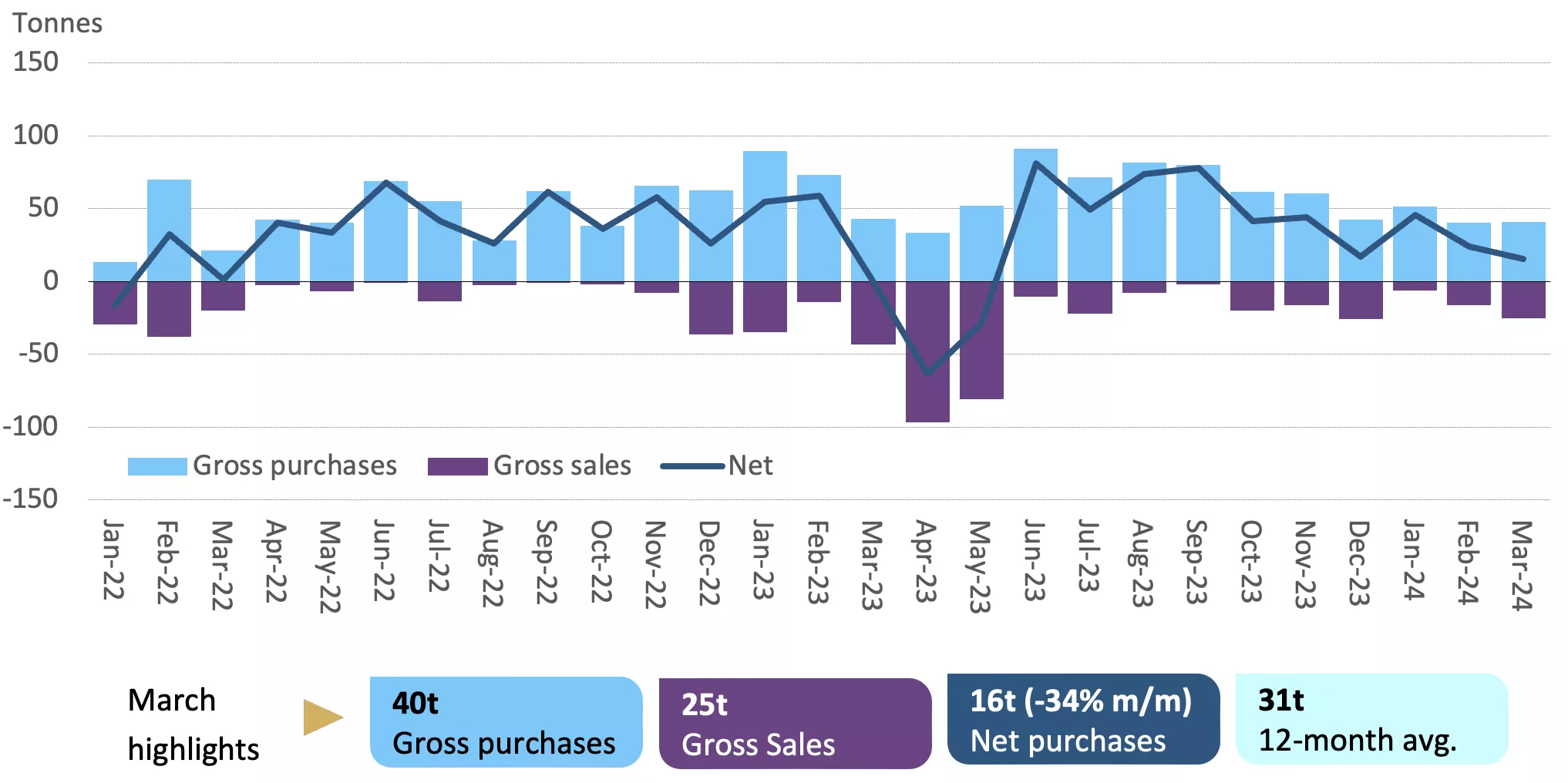

16t of net purchase was reported by central banks in March to the IMF and other open data sources.

Demand was strong as seen by the consistent monthly gross purchases of 40t, partially offset by 25t in gross sales.

March Changes On Gold Price FintechZoom by country

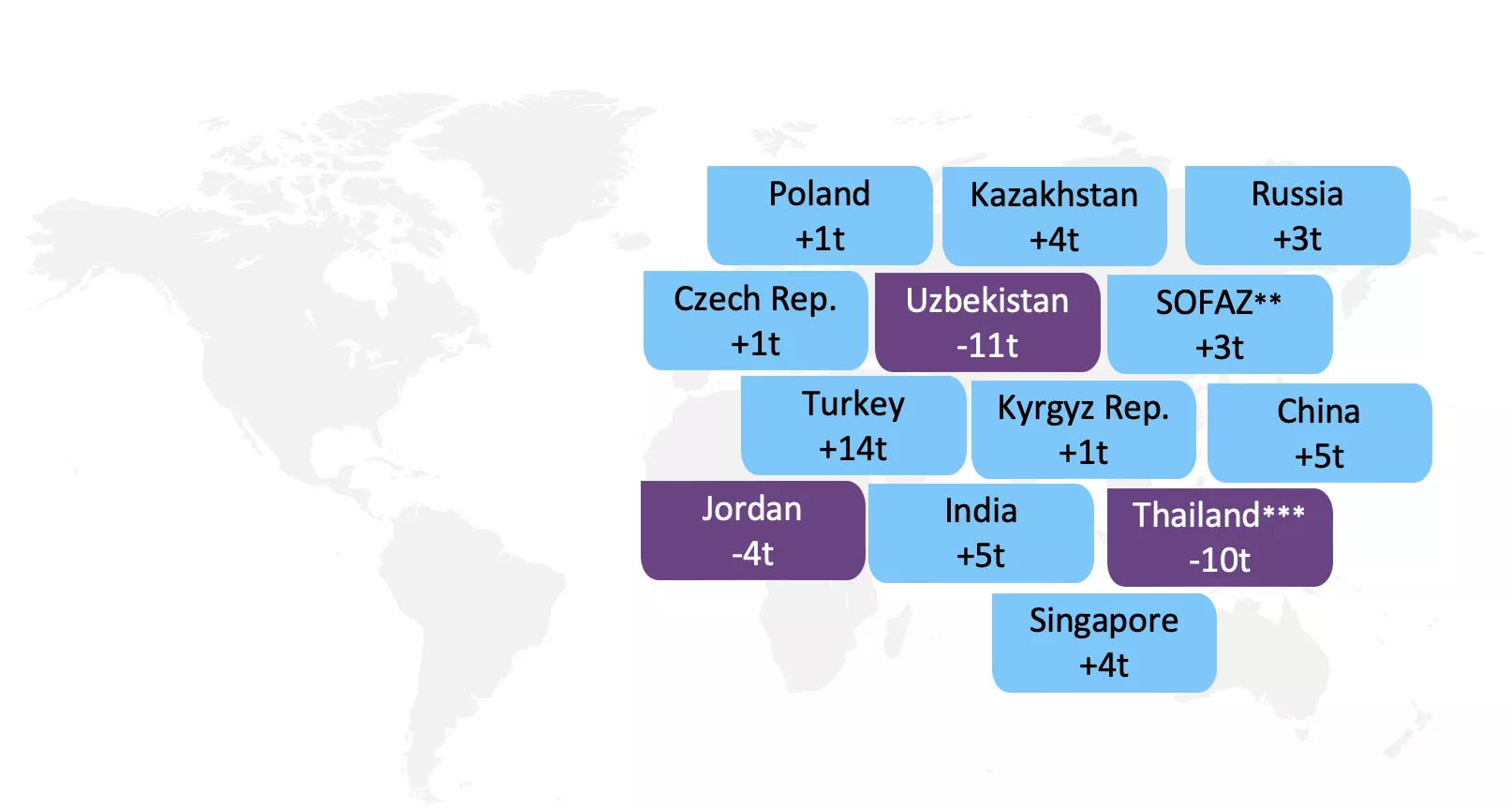

The central banks that have been active recently lead the trades in March.

Every significant customer came from an emerging market. The Reserve Bank of India, the People’s Bank of China, and the Central Bank of Turkey were the next banks to add the most gold during the month (14t).

**From January to March of 2024, the Republic of Azerbaijan’s State Oil Fund had a 3t growth in its gold reserves. ***This has to do with a change in reporting to only include gold that is at least 995/1,000 pure. The quantity of gold shown in BOT’s Financial Statements as Net Foreign Assets is unaffected by this.

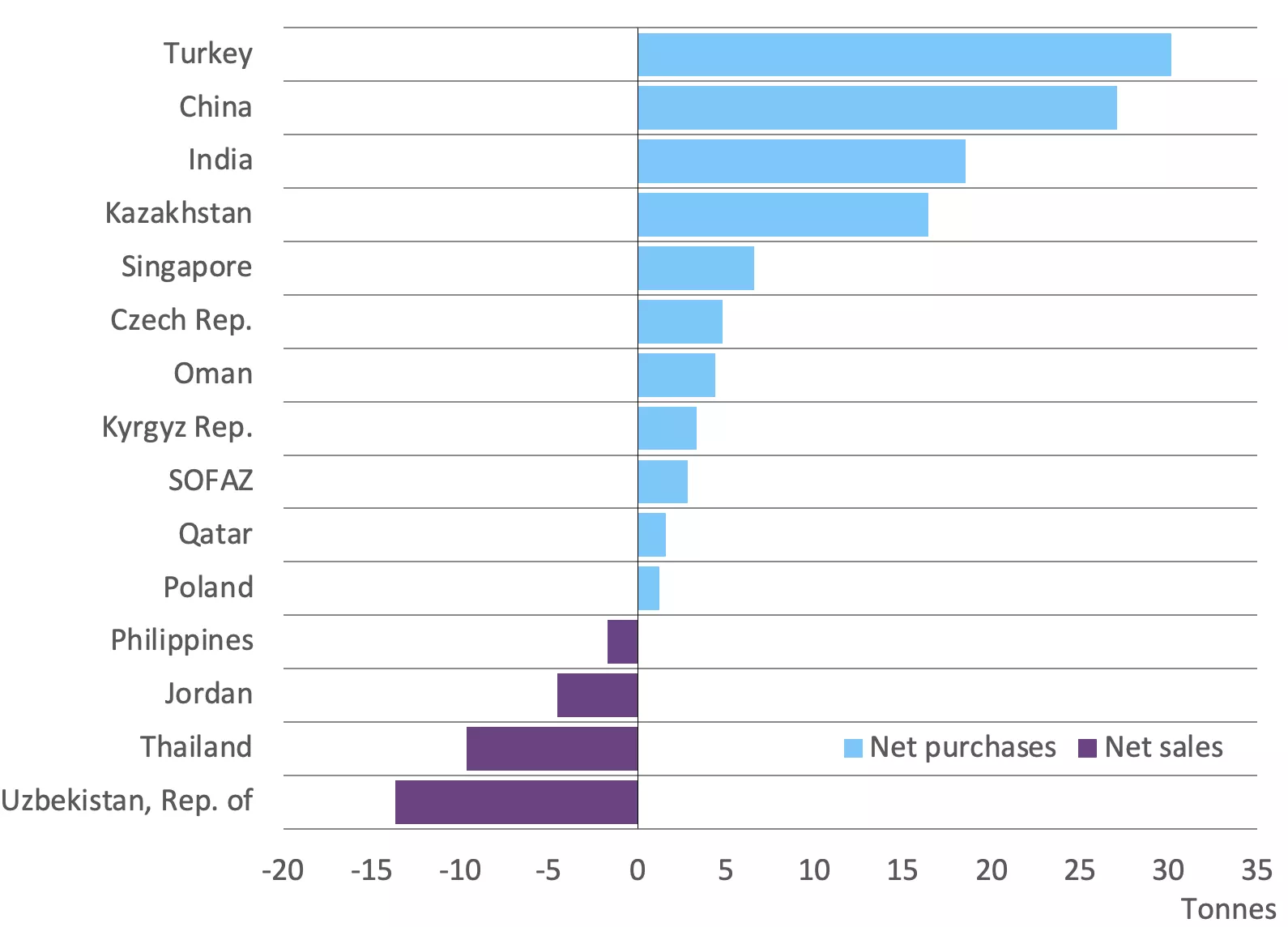

Year-To-Date Changes On Gold Price FintechZoom By Country

Up until 2024, buying strength persisted, with emerging market banks acting as the primary catalyst for both sales and acquisitions.

The only developed market bank increasing its gold reserves is the Monetary Authority of Singapore.

Being the only sovereign wealth fund to disclose growing its gold holdings by 3t y-t-d makes SOFAZ noteworthy.

China’s Gold Price Fintechzoom In April: Investment Demand Getting Strong

Key Highlights:

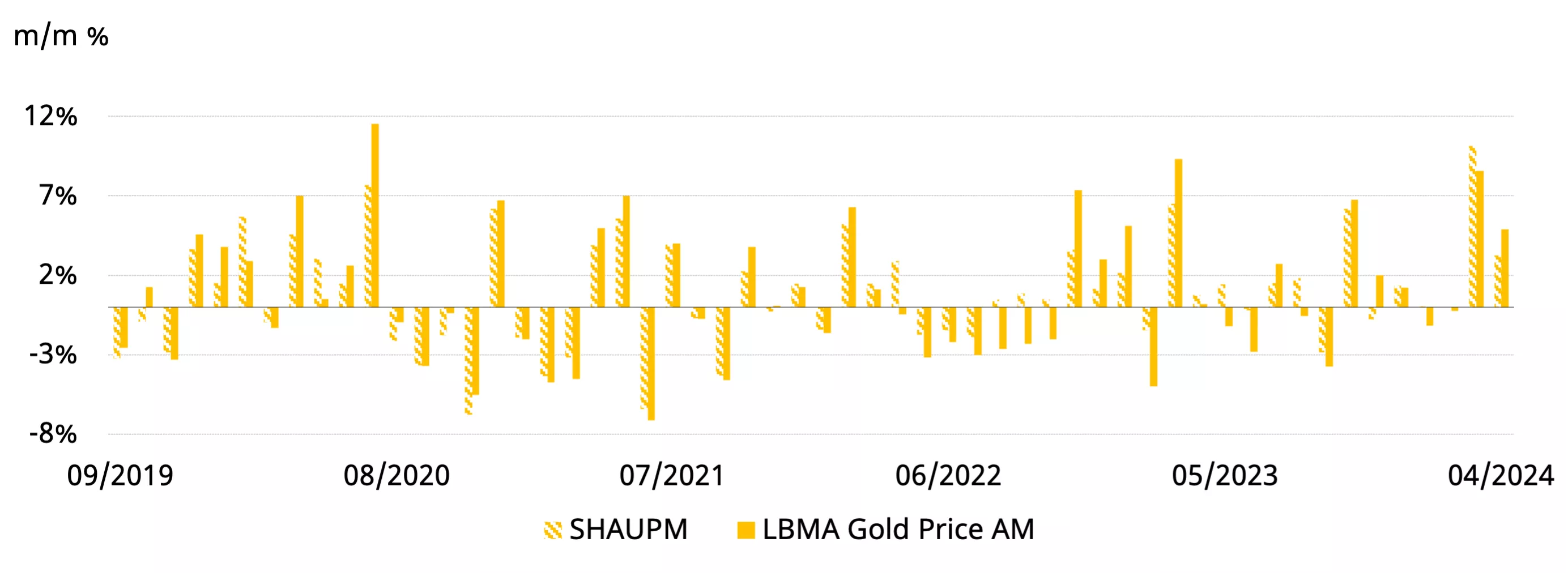

- Both the LBMA Gold Price AM in USD and the Shanghai Gold Price FintechZoom Benchmark PM (SHAUPM) in RMB maintained their momentum in April, recording additional increases.

- The amount of gold removed from the Shanghai Gold Exchange (SGE) in April was 131t, up 7t month over month and 10t year over year: strong demand for investments mitigated the downturn in gold jewelry

- The average local gold price premium increased month over month in line with trends in China’s wholesale gold demand.

- April saw the largest-ever monthly inflow of RMB9 billion (+US$1.3 billion, +17t) into Chinese gold ETFs, marking their fifth consecutive month of inflow; holdings and total assets under management (AUM) also returned to all-time highs.

- For the past eighteen months, the People’s Bank of China (PBoC) has declared its intention to buy gold. At 2,264t at the end of April 2, official gold holdings represented 4.9% of PBoC total reserves, the largest percentage ever.

Looking Ahead

- Industry conversations indicate that during the five-day Labor Day holiday in early May, there was lukewarm demand of gold jewelry because consumers were put off by the elevated price of gold. In the meantime, investors stayed away from the market in late April and early May due to the volatility of the gold price, ostensibly waiting for a more definite price trend.

- Future jewelry demand might continue to be weak due to seasonality and the high price of gold. However, we think that despite some signs of weakness, gold investment in China will probably be supported by the ongoing demand for wealth preservation and gold’s current high profile.

April Continued Gold Price FintechZoom Strength

Although more slowly than in March, gold prices increased once more in April (Chart 1). The SHAUPM in RMB increased by less than 3%, however the LBMA Gold Price AM in USD increased by 5%. Increased geopolitical threats and aggressive futures trading were among the factors that supported gold’s gain during the month.

Chart 1: Gold rose further

Monthly changes of SHAUPM and LBMA Gold Price AM*

*Note: Because the trading windows used to determine the LBMA Gold Price AM and SHAUPM are closer to one another than those used to determine the LBMA Gold Price PM, we compare the two. Please visit Shanghai Gold Exchange for additional details regarding Shanghai Gold Benchmark Prices.

Sources: World Gold Council, Shanghai Gold Exchange, and Bloomberg

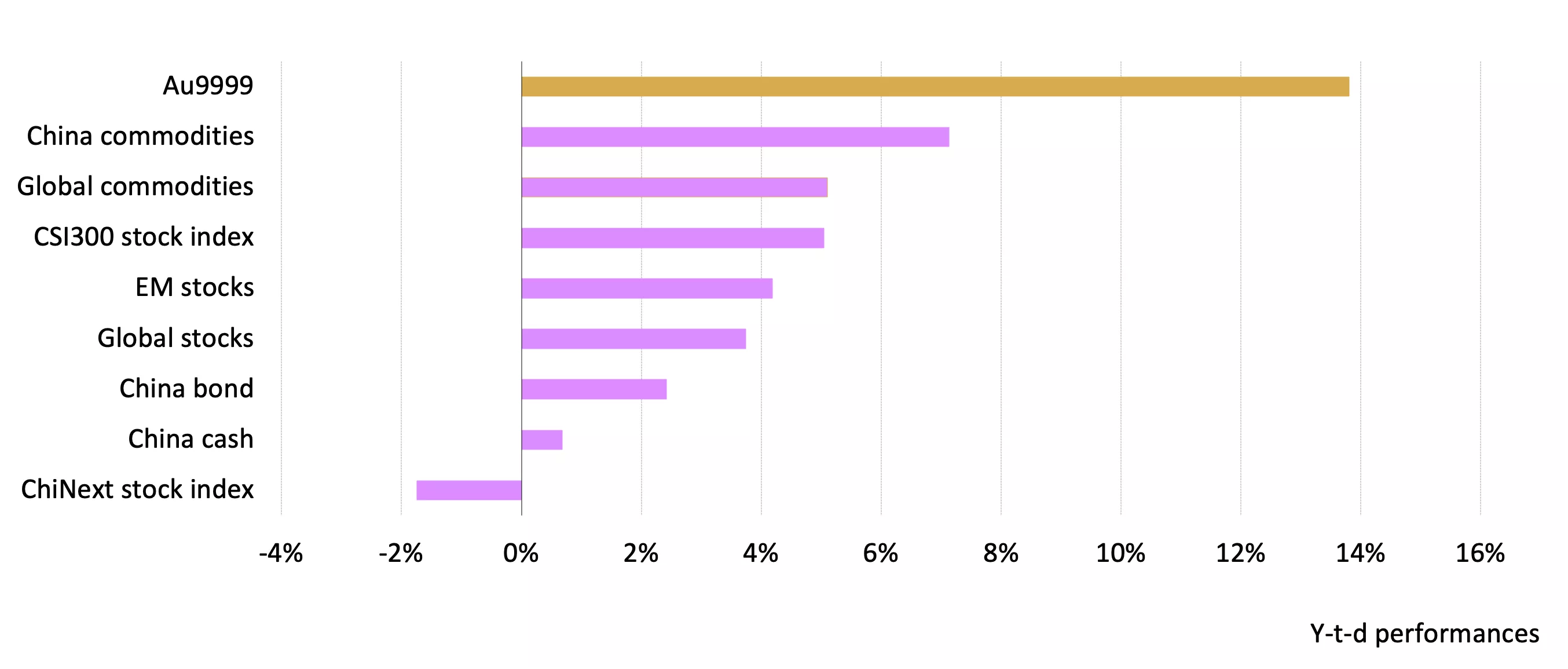

Gold has performed well so far this year in comparison to other significant assets (Chart 2). The RMB gold price rebound in April reached 14% year-over-year and attracted ongoing interest from regional investors.

Chart 2: In April, Gold Price FintechZoom Continued To Rise Year Over Year

Major asset performance so far in 2024*

*As of April 30, 2024; all figures are RMB. CSI China Money Market Fund Index, S&P 500 Index, WTI Crude Oil, Bloomberg US Treasury Aggregate, Bloomberg China Bond Aggregate, Shanghai Shenzhen 300 Stock Index, Wind China Commodity Index, and the ChiNext stock index are the sources of this data.

Sources: World Gold Council, Shanghai Gold Exchange, and Bloomberg

The Demand For Gold Price FintechZoom at Wholesale Increased

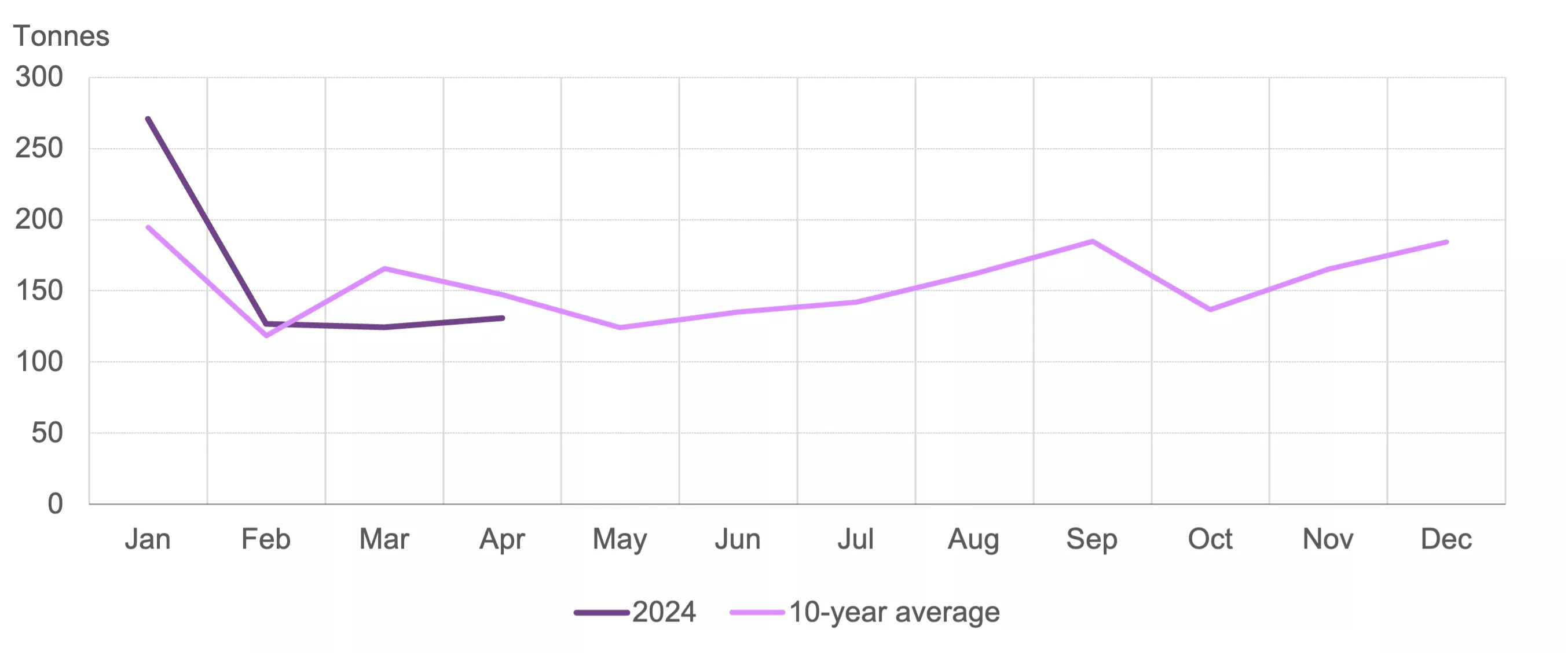

In April, the industry removed 131t of gold from the SGE, which was a 7t increase m/m and a 10t increase y/y (Chart 3). Overall, the demand for gold jewelry was offset by strong investments. Anecdotal data indicates that despite ongoing value preservation needs and the growing price of gold, physical gold investment remained robust, particularly in the first half of April. However, many jewelers were hesitant to restock for the customary Labor Day holiday sales bump due to the strength of the gold price.

Chart 3: SGE Gold Withdrawals Were Sustained By Investment Demand

Gold withdrawals from the SGE in 2024 and the 10-year average*

The Local Premium Followed Patterns In Demand

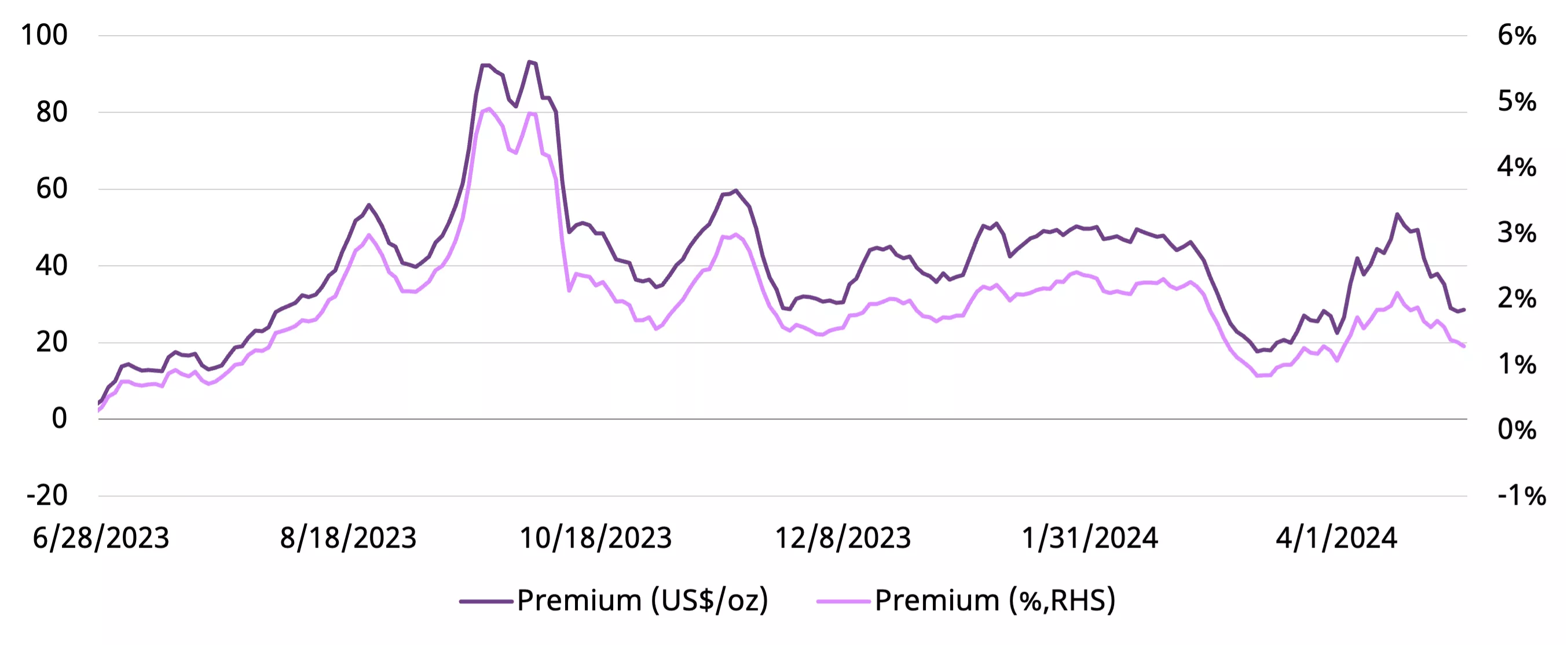

Trends in demand were shown by variations in the premium for gold in the area. The premium for April increased by US$16/oz m/m to US$42/oz (1.7%) on a monthly average basis. A deeper examination also reveals a trend (Chart 4): the price pullback later in the month seems to have dampened momentum, whilst the ongoing price climb in the earlier part of the month increased investment demand.

Chart 4: In April, the local Gold Price FintechZoom premium increased and decreased.

The monthly average spread between SHAUPM and LBMA Gold Price AM in US$/oz and %*

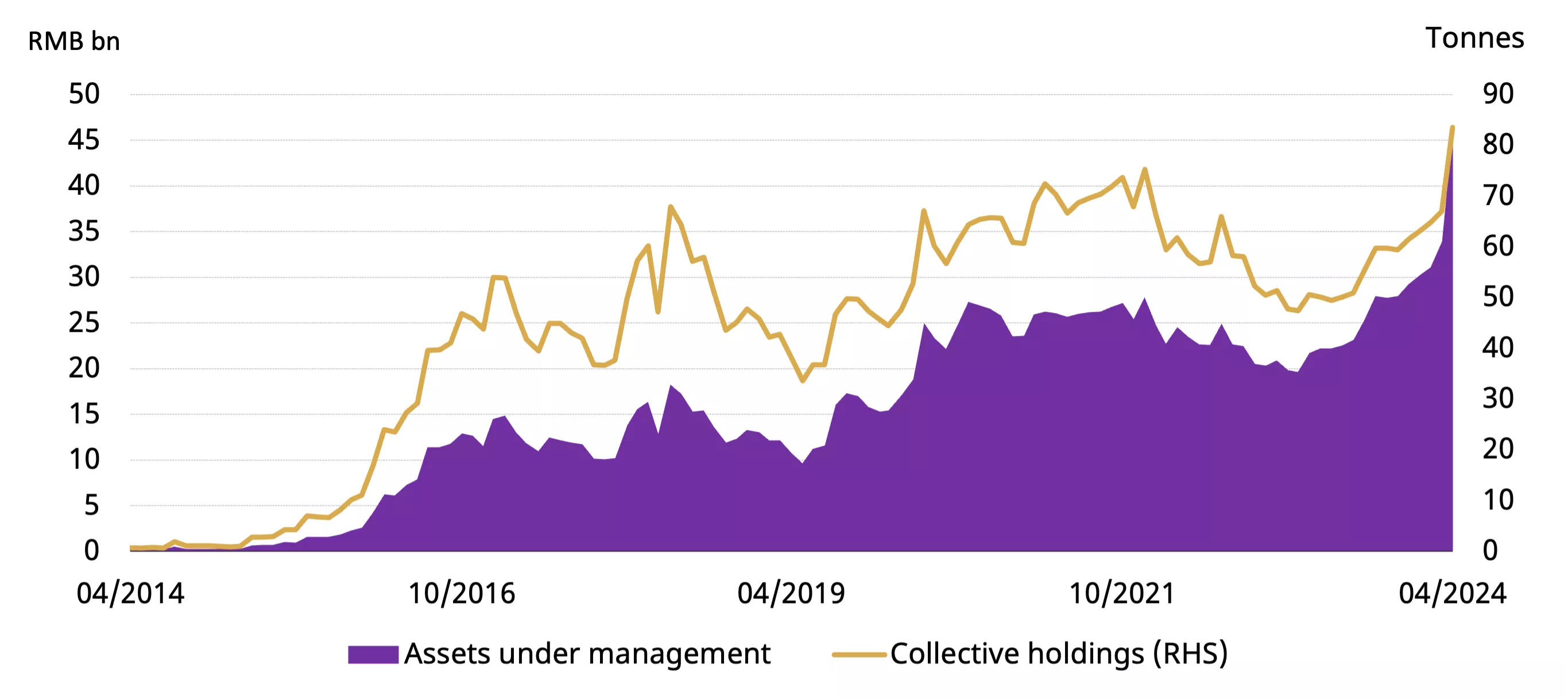

Chinese gold exchange-traded funds saw their highest monthly demand ever.

For the past five months, Chinese gold ETFs have witnessed inflows. The greatest month on record, April brought in RMB9 billion (US$1.3 billion), bringing the overall AUM to a new all-time high of RMB46 billion (US$6.4 billion). In the meantime, holdings increased by the most in a single month, from 17t to 84t (Chart 5). Investor interest in gold was piqued by the metal’s sustained gain, particularly in the first part of April. However, when the momentum in gold prices slowed toward the end of the month, so did Chinese demand for gold ETFs.

Chart 5: The monthly inflow into Chinese gold ETFs was the highest on record

Monthly fund flows and Chinese gold ETF holdings

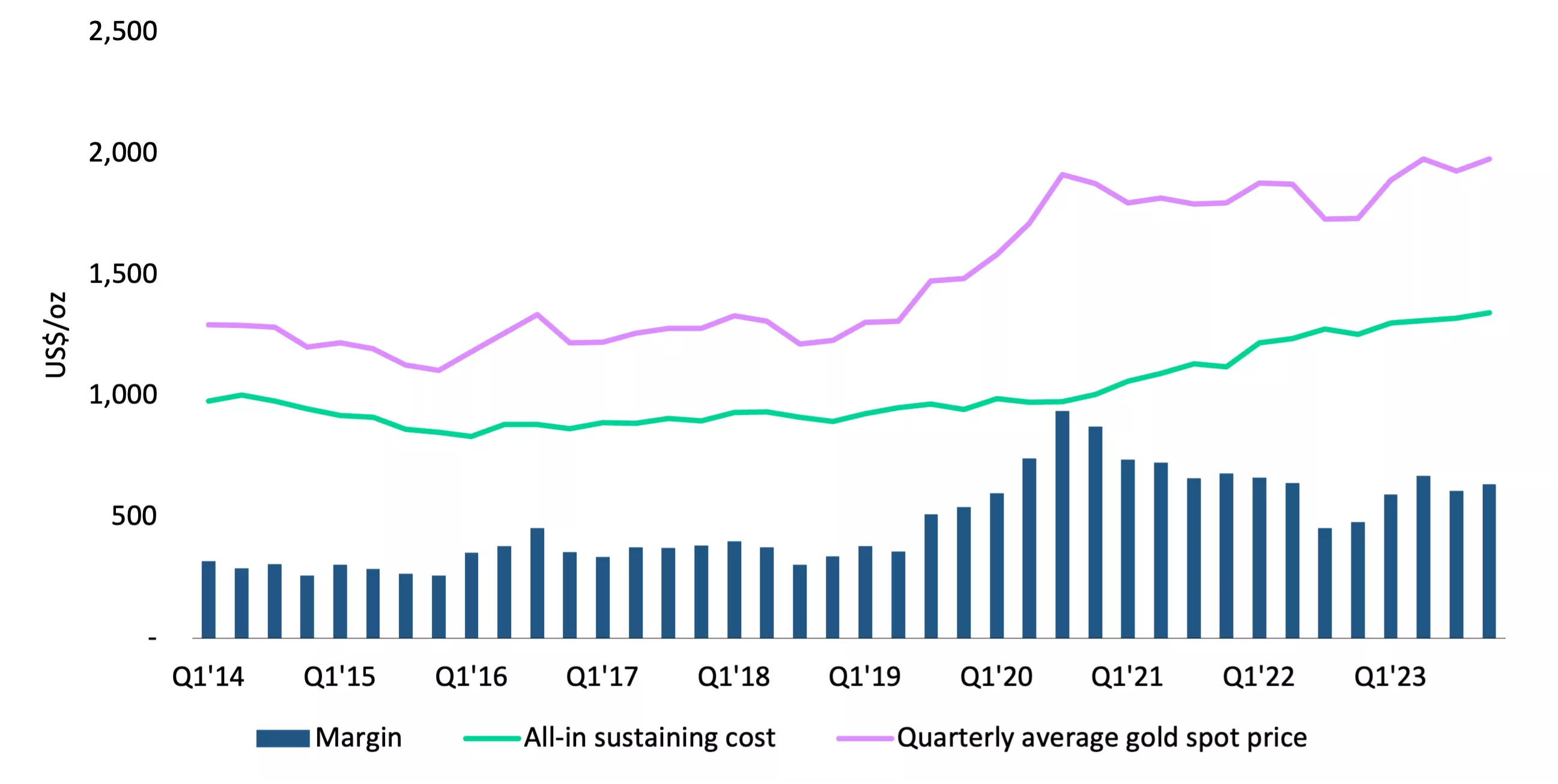

Increased Gold Price FintechZoom Release Producer Margin Pressure

The average all-in sustaining costs (AISC) of gold miners worldwide increased by 2% quarter over quarter to US$1,342/oz in Q4’23 as labor shortages and ongoing cost inflation continued to have an impact on on-site operating expenses. Fortunately, there is some good news: the rate of increase is decreasing, and the pressure on producer margins has lessened due to the increased price of gold. The global average margin in Q4’23 was a reasonably solid US$635/oz, creeping back towards the levels of H1’22 but still a long way off the record margins of 2020 using the quarterly average spot price of US$1,977/oz.

Manufacturer AISC Margins are still rather strong due to the rising price of gold.

Quarterly global average AISC, AISC margins and gold price US$/oz*

Over the year, local inflation decreased in many producer countries. Furthermore, the prices of cyanide, natural gas, and oil all trended lower, which is likely what led to lower operational expenses. However, any advantages were probably outweighed by increased labor costs (caused by the industry’s persistent skills gap), persistently high consumables prices, and the appreciation of local currencies relative to the US dollar. In addition, the cost of protection has increased for businesses that operate in higher-risk areas. As a result, prices keep changing and geographical differences don’t go away.

In Q4’23, North America’s average AISC increased 2% on a quarterly basis to US$1,522/oz. This was the most expensive region overall and maintained the cost-growth trend that started in 2017. The region’s average AISC margin was US$454/oz, up 4% on a quarterly basis but still far less than margins in 2021. At Nevada Gold Mines, Barrick reported a higher q/q AISC, supported by higher Total Cash Costs (TCC) and sustaining capital expenditure. After Q2 and Q3 strike action, Newmont ramped up the mine at Peñasquito, processing lower tonnage and grade, leading to an increase in AISC.

Oceania saw an increase in AISC of 1% q/q to US$1,132/oz. As a result, the average AISC margin increased by 7% on a quarterly basis to US$692/oz. Higher q/q AISC at Tanami and Boddington was reported by Newmont. The company reported greater direct mining expenses at Tanami, and throughout the quarter, poorer grade ore was milled at Boddington. On the other hand, because of improved recoveries and processing of higher grade ore, Evolution Mining posted reduced AISC at its Cowal plant. The quarter for Northern Star Resources was uneven. Because it received the first higher grade ore from Golden Pike North, the KCGM mine had lower AISC, but the Yandal operations saw an increase in AISC due to decreased mill availability.

In Q4’23, South America’s average AISC decreased 3% on a quarterly basis to US$1,372/oz, resulting in an average AISC margin of US$604/oz for the quarter. Higher grades processed and an average TCC of US$998/oz supported the decline in AISC. For the first time since Q4’22, the TCC for the area dropped below $1,000/oz. The AISC profited from increased by-product credits and inventory change at Newmont’s Yanacocha mine in Peru. In contrast, AngloGold Ashanti recorded a higher AISC at Cerro Vanguardia in Argentina due to the substantial impact of severe inflation and the devaluation of the Argentine peso on mine expenses, which the company projected to be 211.4% by year’s end.